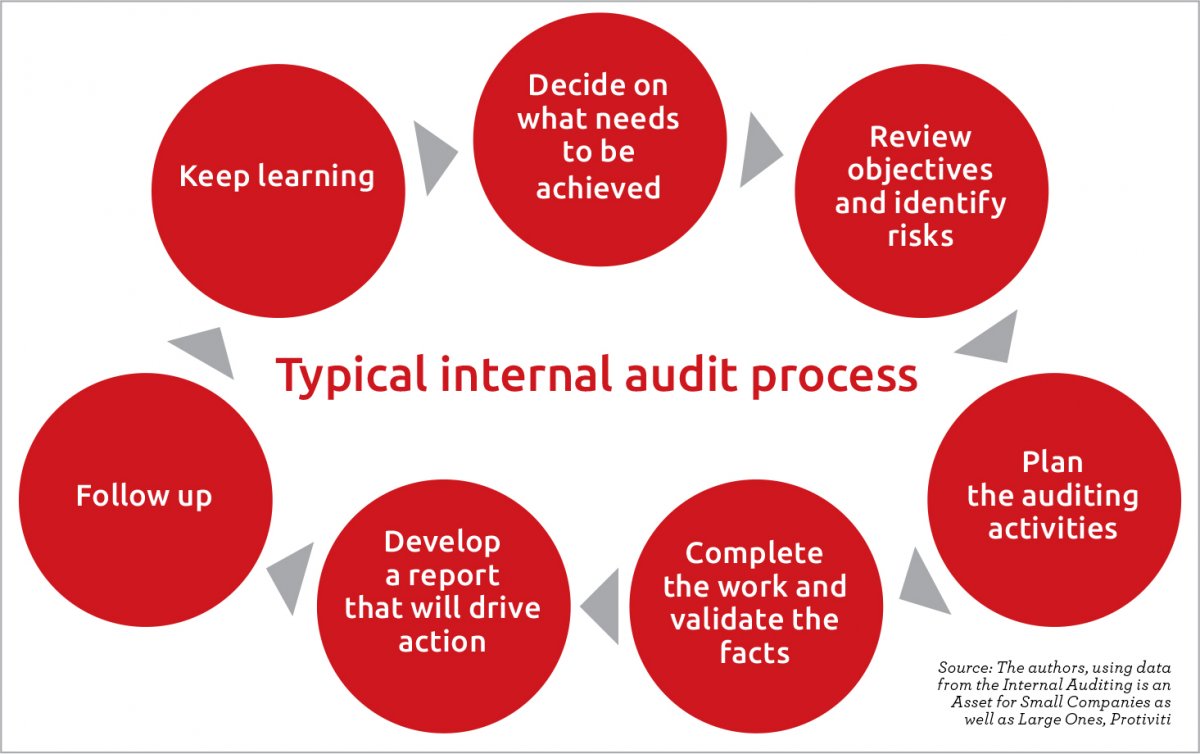

This chapter explains the concept of internal audit in auditing. In big organizations where the business operations takes place from various locations with the workforce of thousand employees, a team of experts review the procedures and operations of an organization and report it to the management in cases such as non-compliance, lack of control and efficiency. The requirement of internal audit team includes expertise in accounting, organizational behaviour and functional areas of management.

Statutory requirement

According to the section 138 of the companies act-

- An internal auditor such as chartered accountant or cost accountant or any other professional is appointed by the board as per the decision to conduct internal audit of the functions and activities of the company

- The amenity and intervals in which the internal audit is conducted and reported to the board is prescribed by the central government by following some rules.

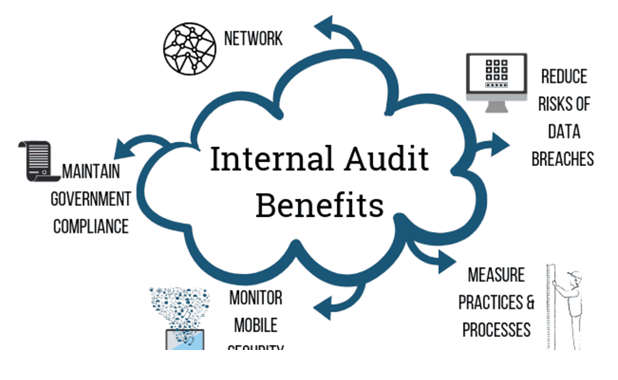

Scope of internal audit

According to the institute of internal auditors, the scope of internal audit is the following-

- Assets safeguarding

- Systematic and economical use of the resources

- Incorruptibility and reliability of the information

- It also includes the accomplishment of the established goals and objectives for programs or operations

Objectives of internal audit

The main objectives of internal audit are the following-

- To comment about internal control system’s effectiveness in force

- To grant proposals about internal control system’s improvement in the organization

- To ensure and check whether the policies and procedures are being followed or not which are laid down by the top management

- To check whether the assets of organization are accounted and safeguarded properly

- To ensure whether the organization follows the standard accounting practices or not

- Discernment and avoidance of errors and frauds at the earliest

- To ensure the authenticity, correctness and accuracy of financial accounting

- To investigate at the management’s special request

- To check the validity and legitimacy of the liabilities of organization

Internal check and internal audit

Internal check is the positioning of the duties of staff members in such a manner that the work performed by an individual is checked by the other automatically and independently.

Internal audit, on the other hand, is a review of various records and operations of the company by the specially appointed staff.

The scope of internal audit is much wider as compared to that of internal check.

More number of employees is involved in the internal check system as compared to the internal audit.